PF contributions are the monthly amounts that an employee and their employer deposit into the employee’s Provident Fund account. Both sides contribute 12% of the employee’s basic salary plus dearness allowance (DA). The Employees’ Provident Fund Organisation (EPFO) manages these funds, pays annual interest on them, and releases the money at retirement or during approved life events.

That is the short answer. However, there is more to it than a single percentage. The employer’s share is split across three schemes. The rules changed in 2026 with a brand-new EPF Scheme. Moreover, the interest rate, wage ceiling, and withdrawal rules all affect how much you actually take home.

In this guide, we break down PF contributions in simple language – for employees who want to understand their payslip, and for HR and payroll teams who need to stay compliant.

What Is a PF Contribution?

A PF contribution is a mandatory monthly deposit into an employee’s Employees’ Provident Fund (EPF) account. The employee contributes 12% of basic salary + DA, and the employer matches it with another 12%. Together, this money builds a retirement corpus that earns tax-free interest every year.

The Provident Fund system in India was originally governed by the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. In 2026, however, the government notified the Employees’ Provident Fund Scheme, 2026 under the Code on Social Security, 2020. As a result, the legal framework is new, but the core structure of contributions remains the same.

Who does it apply to? Any establishment with 20 or more employees must register with EPFO. Smaller organizations can also join voluntarily.

Employee EPF Contribution: How Much Is Deducted from Salary?

The employee EPF contribution is 12% of basic salary plus dearness allowance. This entire 12% goes directly into the employee’s EPF account. Nothing is diverted elsewhere.

For example, if your basic salary + DA is ₹20,000, your monthly PF deduction is ₹2,400.

In addition, employees who want to save more can use the Voluntary Provident Fund (VPF). Through VPF, you can contribute beyond the mandatory 12% – up to 100% of your basic salary + DA and earn the same EPF interest rate on it. The employer, however, is not required to match anything above 12%.

Employer PF Contribution: Where Does the 12% Actually Go?

The employer PF contribution is also 12% of basic + DA. However, unlike the employee’s share, it is split across three schemes:

Component | Rate | What It Covers |

Employees’ Provident Fund (EPF) | 3.67% | Retirement savings |

Employees’ Pension Scheme (EPS) | 8.33% (capped at ₹1,250/month) | Monthly pension after 58 |

Employees’ Deposit Linked Insurance (EDLI) | 0.50% | Life insurance cover |

EPF Administrative Charges | 0.50% | EPFO administration |

Two important points here. First, EPS contributions are calculated only on a wage ceiling of ₹15,000. So the maximum EPS diversion is ₹1,250 per month (8.33% of ₹15,000). Any balance from the employer’s 12% flows back into EPF. Second, EDLI and administrative charges are paid over and above the 12%. Therefore, the employer’s total outflow is roughly 13% of the employee’s PF wages.

This also answers a very common payslip question: the employer’s share in your PF passbook looks smaller than yours because 8.33% of it goes to your pension account, not your EPF account.

Is PF Contribution Mandatory for Salary Above ₹15,000?

PF contribution is mandatory for employees earning basic + DA up to ₹15,000 per month. Above that limit, membership becomes optional, but only in one specific situation.

A first-time employee earning more than ₹15,000 (basic + DA), who has never held a PF account before, can opt out by submitting Form 11 at joining. Such a person is called an “excluded employee.” However, once even a single PF contribution is made, opting out is no longer possible. Membership continues for the rest of your career, though contributions can be restricted to the ₹15,000 ceiling.

The EPF Scheme, 2026 has now stated this rule more explicitly: the 12% mandatory contribution applies only up to the ₹15,000 wage ceiling. Contributions on wages above that remain a voluntary choice between the employer and employee.

How Is PF Contribution Calculated? (With Example

Let’s take an employee with basic salary + DA of ₹15,000 per month:

Contribution | Calculation | Amount |

Employee EPF contribution | 12% × ₹15,000 | ₹1,800 |

Employer EPS contribution | 8.33% × ₹15,000 | ₹1,250 |

Employer EPF contribution | 3.67% × ₹15,000 | ₹550 |

Total monthly PF deposit |

| ₹3,600 |

If the salary is higher, say ₹30,000, the employee still contributes 12% on the full amount (₹3,600). The employer’s EPS share, however, stays capped at ₹1,250, and the remaining ₹2,350 goes into EPF.

What Is the EPF Interest Rate for FY 2025-26?

EPFO has notified an interest rate of 8.25% per annum for FY 2025-26, approved by the Ministry of Labour and Employment. The rate is unchanged from the previous year and applies to all contributions in the financial year.

Interest is calculated monthly on the running balance but credited once a year, at the end of the financial year. Notably, EPS contributions do not earn interest, that portion of funds is instead invested in your pension.

On the tax side, employee contributions qualify for deduction under Section 80C (up to ₹1.5 lakh). Interest is tax-free as well, except on employee contributions above ₹2.5 lakh in a financial year.

What Changed Under the EPF Scheme, 2026?

The EPF Scheme, 2026 replaced the 1952 framework in July 2026 as part of the new labour codes. For most employees, nothing changes in day-to-day terms. Your UAN, balance, service history, and interest rate all continue as before. Still, a few updates matter:

- Contribution rates stay the same.12% employee + 12% employer, with the reduced 10% rate continuing for eligible small and notified establishments.

- Simpler withdrawals.Thirteen separate provisions regarding withdrawal have been simplified into three main categories – basic requirements (health, education, marriage), property related, and special cases. A 25% minimum retention policy has been adopted for partial withdrawals before retirement.

- Stricter rules for private PF trusts.Exempted establishments must now maintain electronic records, offer online account access, and settle claims within prescribed timelines.

Alongside the scheme, EPFO is rolling out EPFO 3.0, a major digital upgrade. The auto-settlement limit for claims has been raised from ₹1 lakh to ₹5 lakh. Furthermore, UPI and ATM-based PF withdrawals have been announced, along with face authentication on the UMANG app and Aadhaar-based KYC updates.

PF Contribution Rules for Employers: ECR, Due Dates, and Penalties

For employers, PF compliance runs through the ECR (Electronic Challan-cum-Return) — the monthly return filed on the EPFO employer portal that lists every employee’s wages and contributions.

Here is what compliance looks like each month:

- Deduct 12% from each eligible employee’s PF wages during payroll.

- Add the employer’s share (12% + EDLI +admincharges).

- File the ECR and deposit the full amount by the 15th of the following month.

Miss the deadline, and the costs add up quickly. Late deposits attract interest of 12% per annum, plus damages that increase with the length of the delay. Beyond penalties, delayed contributions show up as missing entries in employees’ PF passbooks — which directly damages trust.

This is where payroll automation earns its keep. An HRMS like Zimyo calculates PF on every salary structure automatically, generates ECR-ready files, and keeps a record of every filing. Consequently, HR teams spend less time reconciling challans and more time answering the questions that matter.

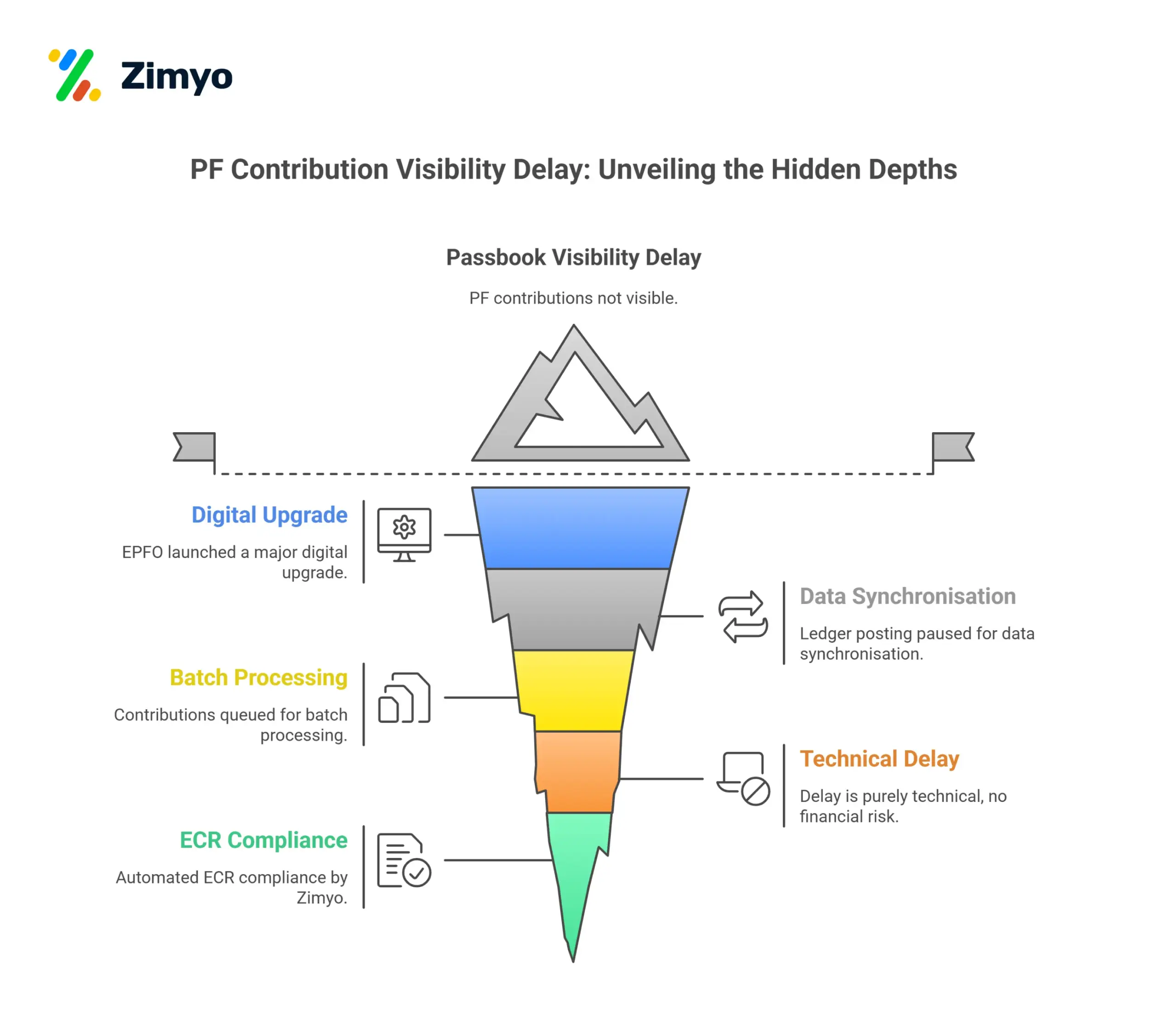

Why Is My PF Contribution Not Showing in the Passbook?

If a recent PF contribution is missing from your passbook, the most likely reason is an EPFO system update, not a missed deposit by your employer.

During 2025-26, EPFO migrated to a new ledger and database architecture. Passbook entries are now posted in batches, so recent contributions can take several days to appear, especially after portal maintenance windows. Your money remains safe, keeps earning interest, and the entries appear automatically once processing clears.

Meanwhile, you can verify your balance without the passbook: give a missed call to 011-22901406 from your registered mobile number, use the UMANG app, or ask your HR team for the ECR filing confirmation.

Conclusion

PF contributions are simple at the surface – 12% from you, 12% from your employer — but the details decide the outcome. The EPS split, the ₹15,000 ceiling, the 8.25% interest rate, and the new EPF Scheme, 2026 – all shape how your retirement corpus grows. For employees, the takeaway is to check your passbook regularly and understand where each rupee goes. For employers, the takeaway is timeliness: accurate ECR filings by the 15th of every month, without exception.

Automating that process removes the risk entirely. Zimyo’s payroll software handles PF calculation, ECR generation, and statutory compliance out of the box, so contributions land on time, every time.

Frequently Asked Questions (FAQs)

What is the PF contribution rate in 2026?

The PF rate payable by an employee is 12% of basic pay plus DA, while the rate payable by the employer is 12%. Some selected institutions, like those having less than 20 workers, have a contribution rate of 10%. These rates remain the same under the EPF Act, 2026.

What is the employer PF contribution breakup?

From the 12% that the employer contributes, 8.33% is contributed towards the Employee’s Pension Scheme (with a maximum contribution of ₹1,250 per month), while 3.67% is paid into the EPF account. In addition, the employer pays 0.5% for EDLI and 0.5% as administrative charges.

Is PF contribution mandatory if my salary is above ₹15,000?

It is only optional for the first-time members who have never held a PF account before. They can choose not to be a part of it by filling up Form 11 when they join. But once you become a PF member, contribution becomes mandatory until you leave your job.

What is the EPF interest rate for FY 2025-26?

EPFO has announced 8.25% per annum interest rate for FY 2025-26. Monthly calculation takes place on the basis of outstanding balance but it gets credited to your account only after the completion of the financial year.

Why is my employer's PF contribution lower than mine in the passbook?

Because 8.33% of the total 12% that the employer contributes goes into the employee’s pension account (EPS). The contribution that shows up in your EPF passbook amounts only to 3.67%, whereas your entire 12% goes into the EPF account.

What happens if an employer delays PF contributions?

Late deposits will attract an interest charge of 12% per year along with penalty charges which increase depending on the delay period. EPFO can also initiate legal proceedings. Employees should make the contribution deposit and ECR filing within the 15th day of every month.

Provident Fund | Meaning and Definition

How to Prepare for a Payroll Data Migration?

Electronic Challan cum Return | Meaning

Arrear | Meaning and Definition

EPFO Increases Withdrawal Limits up to ₹1 Lakh

Is EPF Deductible on Wages Earned on National Holidays in India?

Voluntary PF | Meaning and Definition

Form 11 – Definition & Benefits

Universal Account Number (UAN) | Meaning & Definition

Amendments to the Employees Deposit Linked Insurance Scheme (EDLI)

A Provident Fund (PF) contribution is a mandatory payroll deduction that builds a retirement corpus for employees. Under the Employees’ Provident Fund Organisation (EPFO), both the employee and the employer allocate a fixed percentage of the basic salary to the employee’s PF account each month. These contributions are pooled, earn statutory interest, and become withdrawable upon retirement, resignation, or specific life events, providing a reliable financial safety net.

PF Contributions in 2026: the EPFO has introduced revised contribution slabs that increase the employee share from 12% to 13% of basic wages, while the employer portion remains at 12%. This adjustment aligns with inflation trends and aims to enhance the long‑term savings potential for the workforce. Employers must update their payroll software to reflect the new rates before the 1 January 2026 implementation deadline.

Compliance with the new EPFO rules requires timely reporting through the online portal. Employers must submit revised contribution statements by the 15th of each month, and any shortfall will attract a penalty of 2% per month on the outstanding amount. Additionally, the EPFO has mandated electronic verification of employee bank details to ensure accurate credit of the accrued interest and prevent delays in fund accessibility.

The updated framework offers several advantages: employees benefit from a larger retirement pool, while employers demonstrate adherence to statutory obligations, reducing the risk of legal disputes. To stay ahead, businesses should conduct a payroll audit, train HR personnel on the new guidelines, and communicate the changes clearly to staff. Proactive planning will ensure seamless integration of the new PF contribution structure.