In India, employees are not merely paid salaries at the end of the month. Employers have to adhere to a broad spectrum of labor laws, tax laws, and labor regulations as well. All these laws are referred to as payroll compliance.

Payroll compliance in India entails making sure employee salaries, tax deductions, benefits such as PF/ESI, bonuses, gratuity, and maternity benefits are processed according to government regulations. Disregarding these legal specifications can put businesses at risk of heavy fines, lawsuits, or loss of reputation.

For payroll and HR teams, staying abreast of evolving policies can be challenging. This is why organisations now are moving towards automation with the help of payroll compliance services in India to achieve precision and efficiency.

This blog will cover all you need to know about payroll and compliance; what it is, why you need it, the danger of neglecting it, to a complete compliance checklist.

What is Payroll Compliance?

Payroll compliance refers to adherence to all the legal rules and regulations in handling employees’ payroll. In other words, it is ensuring that:

- Workers are paid just wages under the Minimum Wages Act, 1948.

- Employers are deducting the correct Tax Deduction at Source (TDS) according to income tax regulations.

- Deductions are deposited into schemes such as Provident Fund (PF) and Employees’ State Insurance (ESI).

- Employee perks such as gratuity, maternity leave, and bonuses are provided as required by law.

Payroll compliance also entails keeping proper records of payroll and filing returns with authorities in a timely manner.

Significance of Payroll Compliance

For Employees

Payroll compliance safeguards employees’ rights and their financial stability. Some advantages include:

- Prompt and equitable remuneration: Employees are guaranteed payment of their wages in time, without unlawful deductions.

- Social security benefits: PF, ESI, and gratuity provide financial security to employees at retirement, illness, or in case of emergencies.

- Equal opportunities: Legislation such as the Equal Remuneration Act, 1976 ensures equal pay for equal work.

- Workplace trust: Payroll compliance provides trust among the employer, the employee, and the organization as a whole.

For Employers

For companies, payroll compliance is also crucial. It assists in:

- Prevention of penalties and litigation: Failure to comply may lead to imprisonment, fines, or both.

- Retaining reputation: A compliant payroll system earns trust with clients, employees, and investors.

- Efficient HR processes: Payroll and compliance eliminate conflicts and provide a predictable HR payroll process.

- Staff retention: A compliant payroll demonstrates to employees that the organisation is concerned about their welfare.

Importance of Compliance in Payroll

Payroll compliance is the core of employee payroll management systems. Payroll errors can incur huge costs on businesses without compliance. For instance, non-adherence to the Payment of Bonus Act, 1965 may attract legal action by employees.

Compliance in payroll also ensures:

- Transparency in salary practices.

- Proper tax and contribution deductions.

- Fewer grievances from employees.

- A solid employer-employee relationship.

Risk of Non-Compliance

Lagging in meeting payroll tax compliance and other regulations puts companies under several risks:

- Legal risks: Incompliance with acts such as EPF, ESI, or TDS regulations can result in penalties or jail time.

- Financial penalties: Severe financial penalties can be levied by authorities, putting added cost pressure on companies.

- Employee dissatisfaction: Payroll mistakes decrease employee confidence and can cause increased attrition.

- Reputation loss: Information travels fast, and having the reputation of a non-compliant employer impacts brand credibility.

- Interference with business: Court proceedings and government action can slow down or stop business operations.

Benefits of Payroll Compliance

Here are the top benefits of being compliant in payroll:

Ensures Retention of Employees

Employees are more apt to remain with the business if they observe that salaries, benefits, and tax deductions are done professionally. Payroll compliance has a direct influence on employee retention.

Shields Business from Litigation

Adhering to payroll compliance in India helps shield the business from lawsuits, legal lawsuits, and fines. Compliance also ensures smooth and trouble-free audits.

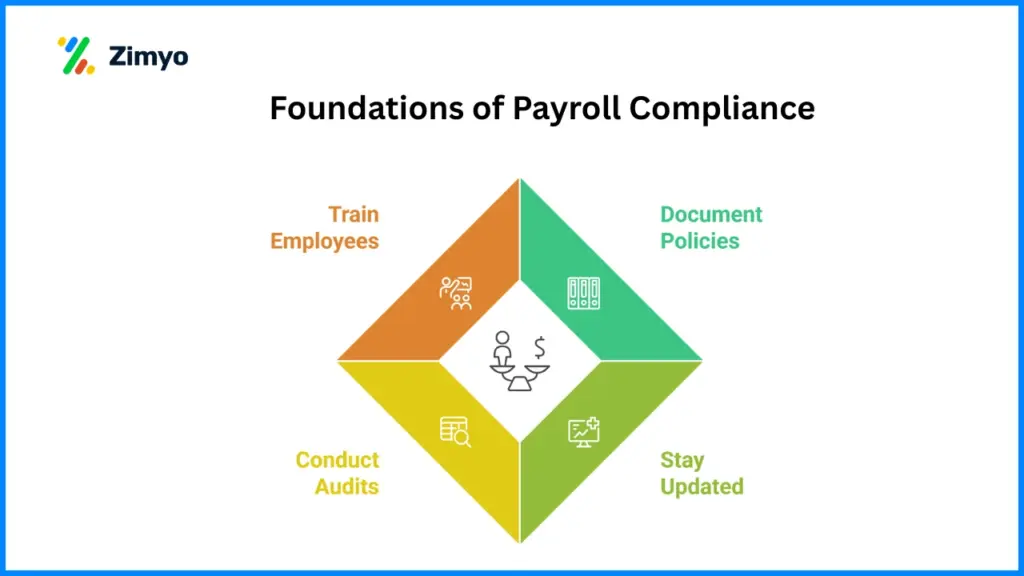

How do you maintain Payroll Compliance for your Organisation?

Compliance is not a choice, it’s a requirement. Here are useful steps companies can follow:

1. Document all policies & procedures

- Have clear written policies for payroll, leave, bonuses, and benefits.

- Documentation serves as proof during disputes or audits.

2. Stay updated on changing Acts and Policies

- Labour and tax laws change frequently. Employers must keep track of government notifications.

- Subscribing to payroll compliance services in India can help in staying compliant.

3. Conduct compliance audits

- Regular audits ensure payroll records, tax deductions, and benefits are accurate.

- Audits identify mistakes early and prevent penalties.

4. Train employees

- HR and payroll staff should receive proper training on laws like the Payment of Wages Act or TDS rules.

- Trained employees reduce compliance risks.

Payroll Compliance Checklist

Payroll compliance for companies in India is not merely a matter of processing wages, it is a matter of aligning payroll procedures with labour laws, tax regulations, and employees’ welfare acts. To assist you, here’s an extensive payroll compliance checklist which every payroll and HR team needs to adhere to:

1. Government Rules for Payroll Compliance

Each company has to comply with central and state legislation. Certain important requirements are:

- Company registration with the concerned labour and tax authorities.

- Retaining statutory records like employee registers, wage slips, attendance records, and bonus registers.

- Filing monthly, quarterly, and yearly returns for PF, ESI, TDS, and labour laws.

- Displaying notices related to compliance at the workplace (like minimum wage notifications).

Adhering to these government regulations creates transparency in payroll and compliance without facing fines.

2. Industrial Relations

The Industrial Disputes Act, 1947

- Regulates retrenchments, layoffs, strikes, and employer-employee disputes.

- Empowers employees against unjust dismissal.

- Compels employers to provide notice and compensation prior to retrenchment.

- Promotes settlement of disputes either by negotiation or through arbitration.

Example: If a company is required to downsize, it is required to comply with procedures under this act to prevent legal consequences.

3) WAGES - what to look out for, what the law states, and examples

A. Payment of Wages Act — timely payment and limits on deductions

What it states (brief): employers have to pay wages in time (normal wage period normally), pay in legal tender/bank, and only deduct the type of deductions the Act permits. The Act further puts limits on overall deductions from wages to safeguard workers: normally 50% of wages for a wage period (and up to 75% where deductions are for approved payments to cooperative societies).

Easy tips for compliance –

- Set a wage-period (typically monthly) and adhere to the payday.

- Record all deductions with employee approval or statutory justification.

- Never take off more than the maximum allowed (50% / 75% rules above).

Example (deduction limit):

If a monthly gross wage of an employee = ₹20,000, the aggregate legally allowed deductions during that wage period (other than extremely limited recoveries) cannot be more than ₹10,000 (50% of ₹20,000). If a deduction is in respect of an approved cooperative society payment it may be as high as ₹15,000 (75%).

B. Payment of Bonus Act — who gets statutory bonus, how it’s computed

Main points:

- Employees earning up to ₹21,000 per month are entitled to a statutory bonus (under other conditions such as minimum workdays). The Act prescribes an 8.33% minimum and 20% maximum statutory bonus. The salary used for computing the bonus is the larger of ₹7,000 or the state floor wage (essentially a limit for most calculations).

How to approach the math (short formula)

- Bonus base = min (employee’s Basic + DA, ceiling), where ceiling = ₹7,000 or state minimum wage (whichever is greater).

- Minimum statutory bonus (monthly) = Bonus base × 8.33%

- (for a whole year, multiply by months worked — in practice a whole-year minimum is about one month’s salary because 8.33% × 12 ≈ 100%).

Worked example (statutory bonus):

- Employee A: Basic + DA = ₹18,000 → eligible (≤ ₹21,000). Bonus base = ₹7,000 (cap).

- Minimum bonus per month = 7,000 × 8.33% = ₹583 → annual minimum ≈ ₹6,997 (if worked whole year).

- Max possible (if company has surplus and pays max 20%) = 7,000 × 20% = ₹1,400 per month → annual ≈ ₹16,800.

C. Minimum Wages Act — state + central rules, classification

What to know:

Minimum wages are prescribed state-wise for various categories of skills (unskilled, semi-skilled, skilled, highly skilled). The central legislation gives the model; the rates and schedules actually fixed and notified by the central or state government for each employment/industry and updated periodically. Employers are required to implement the minimum wage applicable to the work, place and worker category.

Compliance tips

- Have a copy (print or PDF) of the minimum wage notification current for each state.

- For multi-state operations establish payroll regulations by state and job type.

- If you compensate transport allowance, overtime, HRA etc., verify if the state considers them as part of the “wage” for minimum-wage purposes.

Example (how it counts):

If the state minimum wage for an unskilled employee in State X is ₹400/day and you are paying a wage that equates to less than this, you need to raise wages or get fined. Always map every worker onto the proper state schedule (not merely “company policy”).

4) SOCIAL-SECURITY - gratuity, compensation, EPF, ESI, and labour welfare funds (detailed)

A. Gratuity (Payment of Gratuity Act, 1972)

What it says:

- Gratuity is payable on exit after ≥ 5 years of continuous service (exceptions for death/disablement).

- Formula for most workers: Gratuity = (Last month’s salary drawn × 15 / 26) × service years (15 days’ pay for every completed year). The government has set a statutory ceiling that may be paid under the Act (this ceiling has been amended by notification; for several years it has stood at ₹20 lakh — see current notifications for updates).

example (gratuity):

- Last drawn salary (Basic + DA) = ₹50,000 monthly. Years of service = 12 (completed).

Gratuity = (50,000 × 15 / 26) × 12

= (50,000 × 0.576923…) × 12 ≈ (28,846.15) × 12 ≈ ₹3,46,153 (rounding rules apply).

(If the statutory cap is ₹20,00,000 then compare and apply the lower of the two as required by law).

Practical notes

- Keep records of PF/ESI and attendance; these are generally utilized to confirm “last drawn salary” and service years.

- If you provide a superior (contractual) gratuity plan, do so, but ensure legislated minimums are not undercut where the Act holds.

B. Employees’ Compensation (Workplace injury / death)

What it says:

- Under Employees’ Compensation Act, death, permanent total disablement or temporary disablement is payable by a percentage of monthly wages multiplied by an age-related “relevant factor” (Schedule IV) with a minimum amount as set out in the Act. For instance, death: 50% of monthly wages × relevant factor (or minimum amount as set by the Act), and PTD: 60% × relevant factor (or minimum amount), etc.

Worked example (death compensation):

- Monthly wage used for comp. = ₹12,000. Suppose the relevant factor for the worker’s age = 197.37 (example value from schedules).

Compensation for death = 50% × 12,000 × 197.37 = 0.5 × 12,000 × 197.37 ≈ ₹11,84,220 (plus funeral allowance where applicable). (This is an illustrative computation using a sample factor; use Schedule IV to pick the exact factor for the employee’s age.)

Practical tips

- Keep a record of the wages and ages current so that you can simply calculate the “relevant factor” when necessary.

- Most employers purchase workmen’s-compensation insurance to insure this statutory liability.

C. Employees’ Provident Fund (EPF) — basic employer/employee mechanics

What it says (short):

- Statutory contribution is generally 12% of basic pay + dearness allowance from both employer and employee (certain exemptions exist for very small establishments and new employers may choose different schemes under specific rules). The employer’s 12% is split into EPF and Employee Pension Scheme (EPS) components (commonly 8.33% to EPS and 3.67% to EPF — subject to rules and wage ceiling). Check EPFO circulars for exact split and applicability.

Worked example (EPF):

- Basic salary = ₹20,000/month.

Employee contribution (12%) = 20,000 × 12% = ₹2,400 (deducted from salary).

Employer contribution (12%) = ₹2,400 (employer pays), typically split as: EPS 8.33% (₹1,666) + EPF 3.67% (≈₹734) — totals match ₹2,400. (Small rounding differences can occur; employer must follow EPFO rules).

Practical tips

- Use basic + DA as the EPF wage head. If your company uses a higher basic to manipulate PF, be aware EPFO checks for compliance.

- File monthly contributions on time — EPFO enforces penalties for late remittance.

D. Employees’ State Insurance (ESI / ESIC)

What it says:

- ESIC provides coverage to employees in notified establishments earning ≤ ₹21,000 per month (₹25,000 for disabled persons) – observe this wage limit may be altered by notification. The combined contribution as of now is 4% of wages (Employer 3.25% + Employee 0.75%).

Worked example (ESI):

- Monthly gross wage = ₹20,000 (eligible for ESI).

Employee share (0.75%) = 20,000 × 0.75% = ₹150 (deducted).

Employer share (3.25%) = 20,000 × 3.25% = ₹650.

Employer remits total ₹800 (and files the ESI return).

Practical tips

- Register covered establishments timely (ESIC requires registration when employee count crosses thresholds).

- Check whether any allowances (overtime/bonus) are excluded from ESI wage computation per rules.

E. Labour Welfare Fund (state-level)

This is state dependent: a few states have a small wage-based assessment for workers’ welfare; regulations and rates differ. Look at the state labor department or the state labor welfare fund notice for amounts and report. (State notice pages / payroll providers are good quick references.)

5) WOMEN’S BENEFITS — Equal Remuneration & Maternity rules

A. Equal Remuneration Act, 1976

What it requires:

- Employers must pay equally for the same work or work of a similar nature; employers cannot reduce women’s pay or deny benefits because of gender. The Act also prohibits discrimination in recruitment and training if the work is the same. Employers should maintain clear, non-discriminatory salary structures and job descriptions.

Practical compliance steps

- Maintain job descriptions and grading for roles and map pay bands to job grades.

- Use structured pay matrices and document objective criteria for promotions and increments.

- Keep records showing consistent application of pay rules across gender.

B. Maternity Benefit Act (and the 2017 amendments)

Key rules (simple):

- Eligible women who worked 80 days in preceding 12 months get paid maternity leave. After the 2017 amendment: 26 weeks of paid leave for women with up to two surviving children; 12 weeks for women with two or more surviving children. Adoptive mothers and commissioning mothers have 12 weeks. Employers with 50 or more employees must provide crèche facilities and allow up to 4 visits to the crèche during the day. The Act also introduced enabling language for work-from-home arrangements by mutual agreement.

Practical notes and examples

- Salary during leave: Maternity leave is paid based on average daily wage (or normal salary rules in the company) — ensure payroll handles this fully.

- Creche rule example: If your office has 60 employees, you must provide (or arrange) creche facilities and allow the mother four daily visits (this includes rest intervals).

Record keeping and policies

- Advise new hires of maternity benefits in the offer letter as required by law.

- Maintain returns and records for inspections and be ready to provide proof of payments

6) PAYROLL COMPLIANCE ON TAX LIABILITIES — TDS on salary, choosing regimes, and an example

A. Employer obligations under Section 192 (TDS on salary)

Employers must estimate an employee’s taxable salary for the financial year, consider declarations for investments/deductions (Form 12BB and supporting proofs), compute tax liability at the rates in force, and deduct TDS monthly on salary payments (usually 1/12 of annual tax after considering exemptions/deductions). Employers then deposit TDS and file Form 24Q quarterly and provide Form 16 to employees annually.

B. Old vs New tax regime (FY 2024-25)

The new tax regime (section 115BAC) offers lower slab rates but restricts most exemptions/deductions. The old regime allows more deductions (80C, 80D, HRA etc.) but has different slab rates. Employees can choose the regime; employers should collect employee choice/declarations and compute TDS accordingly. The Income Tax Department provides official slab tables and a tax calculator employers can use.

Feature | Old Tax Regime | New Tax Regime (under Section 115BAC) |

Basic exemption / nil tax slab | Up to ₹2,50,000 — no tax | Up to ₹3,00,000 — no tax |

First slab / low income tax rate | ₹2,50,001 to ₹5,00,000 → 5% | ₹3,00,001 to ₹7,00,000 → 5% |

Middle slabs | ₹5,00,001 to ₹10,00,000 → 20% | ₹7,00,001 to ₹10,00,000 → 10% |

Higher slab(s) | Above ₹10,00,000 → 30% | ₹10,00,001 to ₹12,00,000 → 15%; ₹12,00,001 to ₹15,00,000 → 20%; Above ₹15,00,000 → 30% |

Standard deduction | ₹50,000 (for salaried taxpayers) | ₹75,000 (in new regime) |

Rebate under Section 87A | For taxable income up to ₹5,00,000, rebate available (i.e., tax may become zero) | For taxable income up to ₹7,00,000, rebate available (i.e., tax may become zero) |

Exemptions & deductions allowed | Many deductions and exemptions allowed (80C, 80D, HRA, LTA, etc.) | Very limited exemptions/deductions; many typical deductions (like HRA, 80C) are disallowed in this regime |

Important: The government adjusted standard deduction and some slab features in recent budgets, e.g., standard deduction treatment changed for FY 2024-25 (confirm current allowance for the regime used). Always use incometax.gov.in or the tax calculator to compute exact TDS.

Example:

Note: tax laws, rebates and slabs change with budget notifications. The example below uses the official slab structure published for FY 2024-25 and assumes the employee has no other deductions or exemptions except the standard deduction (Old regime = ₹50,000; New regime = ₹75,000 as per the latest FAQs). This is illustrative, actual TDS will differ with HRA, 80C claims, other incomes, and any change in rules.

Scenario: Annual gross salary = ₹12,00,000; no other deductions claimed.

- Old regime assumption: standard deduction ₹50,000; standard old slabs (basic structure).

- New regime assumption: standard deduction ₹75,000; new regime slabs (as notified).

Approximate result (illustrative computation):

- Tax under Old regime (after ₹50,000 standard deduction) ≈ ₹1,63,800 (annual tax after adding 4% cess).

- Tax under New regime (after ₹75,000 standard deduction) ≈ ₹71,500 (annual tax after cess).

So monthly TDS withheld (simple 1/12 rule) would be about ₹13,650 under the old regime vs ₹5,958 under the new regime — again, this is a simplified illustration to show the process and the typical order of magnitude difference; actual employer computation must consider employee declarations and actual rules.

Practical payroll compliance steps for TDS

- Collect declarations early: ask employees for investment proofs and regime choice at year start (Form 12BB for investments / Form for opting new/old regime).

- Use official slabs and tools: run the Income Tax Dept tax-calculator (or payroll tax module) for the correct AY/FY when calculating TDS. Always use the official site for the slab table.

- Apply 1/12th deduction rule: compute annual liability and deduct 1/12 every month (or vary as needed for changes during the year).

- Issue Form 16 timely and deposit TDS on time; late deposits lead to interest and penalties.

- If employees have other income (FD interest, rental, capital gains) instruct them to declare it — employer may need to factor that into the TDS computation (or employees should opt to pay advance tax).

Final practical checklist (quick action items)

- Have copies of relevant central and state notifications for Minimum Wages, Bonus, Gratuity ceilings, EPF regulations and ESI threshold.

- Construct payroll rules (basic, DA, HRA, allowances) so statutory head calculations (EPF, ESI, gratuity base) are automated and audit-friendly.

- Update payroll software when government announces changes (bonus ceiling, gratuity ceiling, standard deduction, tax slabs).

- Train HR and payroll personnel to execute sample calculations each time an amendment is available and maintain archive of previous computations for auditing.

Automate your Payroll Compliance with Zimyo Payroll

Payroll compliance in India is complicated because it involves companies keeping track of several laws, deadlines, and deductions each month. Missing even a tiny step – such as depositing PF a few days behind schedule or submitting the incorrect TDS amount – can lead to penalties and employees losing faith in the organisation. That is why contemporary organisations are shifting towards automation in payroll and compliance.

What Zimyo Payroll does:

- Automated salary processing: Salaries, allowances, overtime, and deductions are auto-calculated with full accuracy.

- Built-in compliance engine: Updates tax rates, PF/ESI rules, and wage regulations automatically.

- One-click filings: Generate and file PF, ESI, and TDS reports in just a few clicks.

- Employee self-service: Staff can access salary slips, tax documents, and Form 16 directly—reducing HR workload.

- Customisation for industries: Whether you run a startup, a manufacturing firm, or an IT company, Zimyo adapts to your compliance needs.

Conclusion

Payroll compliance in India supports hassle-free business operations and employee confidence. From timely salaries to social security benefits, payroll and compliance deal with several laws and acts that serve to protect both employers and employees.

Organisations that neglect compliance risk financial sanctions, employee grievances, and legal issues. However, firms that practice compliance through robust HR payroll measures have a superior reputation, loyal employees, and operational effectiveness.

The most intelligent method of remaining compliant nowadays is to automate compliance using tools like Zimyo Payroll, thus saving time, decreasing errors, and adhering to every law.

FAQs

What is payroll compliance in India?

Payroll compliance in India refers to adhering to labour laws, tax regulations, and employee welfare acts while processing payroll. It ensures timely salary payments, accurate deductions, and statutory filings.

What are the payroll laws in India?

Payroll laws in India include the Payment of Wages Act, Minimum Wages Act, Payment of Bonus Act, Employees’ Provident Fund Act, Employees’ State Insurance Act, Payment of Gratuity Act, and various tax regulations like TDS.

What is payroll compliance?

Payroll compliance means following all statutory rules related to employee wages, benefits, taxes, and deductions, so organisations remain legally compliant and employees are protected.

What are the 5 payroll steps?

The five payroll steps are:

- Collect employee data (attendance, salary, deductions).

- Calculate gross salary.

- Apply statutory deductions (PF, ESI, TDS).

- Disburse net salary.

- File returns and generate compliance reports.

Which is the best payroll software in India?

Zimyo Payroll is trusted by growing businesses for its accuracy, compliance engine, and easy integration. The best payroll software in India is one that automates salary processing, ensures 100% compliance, and reduces manual errors.